Draft ESRS: new standards for sustainability reporting by EFRAG

Earlier, we discussed EFRAG’s consultation on the new European Sustainability Reporting Standards (ESRS for short). Given the many critical responses to the consultation, it remains to be seen whether EFRAG will succeed in submitting the final version of the ESRS to the European Commission in November 2023, as it intends to do.

So the final version may be some time away. Therefore, in this contribution, we take a closer look at the draft ESRS itself: what exactly has EFRAG proposed in it? Compliance is meeting expectations. Using a worked example, we clarify what EFRAG expects from companies in terms of sustainability reporting.

EFRAG has published its full consultation package in English only. When we refer to it, we do so in English and in italics.

The draft ESRS comprise a total of four themes:

Cross-cutting (General)

Environment

Social

Governance

These four themes are again divided into different standards:

two generic standards

five standards for the 'E' (Environment) in ESG

four standards for the 'S' (Social) in ESG and

Two standards for the 'G' (Governance) in ESG

In total, therefore, there are two generic and 11 thematic standards. The first generic standard (ESRS 1) contains three so-called Disclosure Principles for the implementation of policies, objectives, actions, action plans and required resources for sustainability reporting.

All other ESRS contain so-called Disclosure Requirements. In total, there are no less than 137 Disclosure Requirements, all of which are mandatory ("The undertaking shall (...)." This means that, in principle, the undertaking is obliged to report on them. Each Disclosure Requirement in turn consists of sub-themes. Later in this article, we show what that looks like using an example.

All thematic standards have the same structure. They start with the objective of the relevant ESRS and their interaction with other ESRS. This is followed by the elaboration of the Disclosure Requirement, followed by definitions and Application Guidance in annexes. The Application Guidance, which is also formulated in mandatory terms, sets out how companies are expected to apply the Disclosure Requirements in practice.

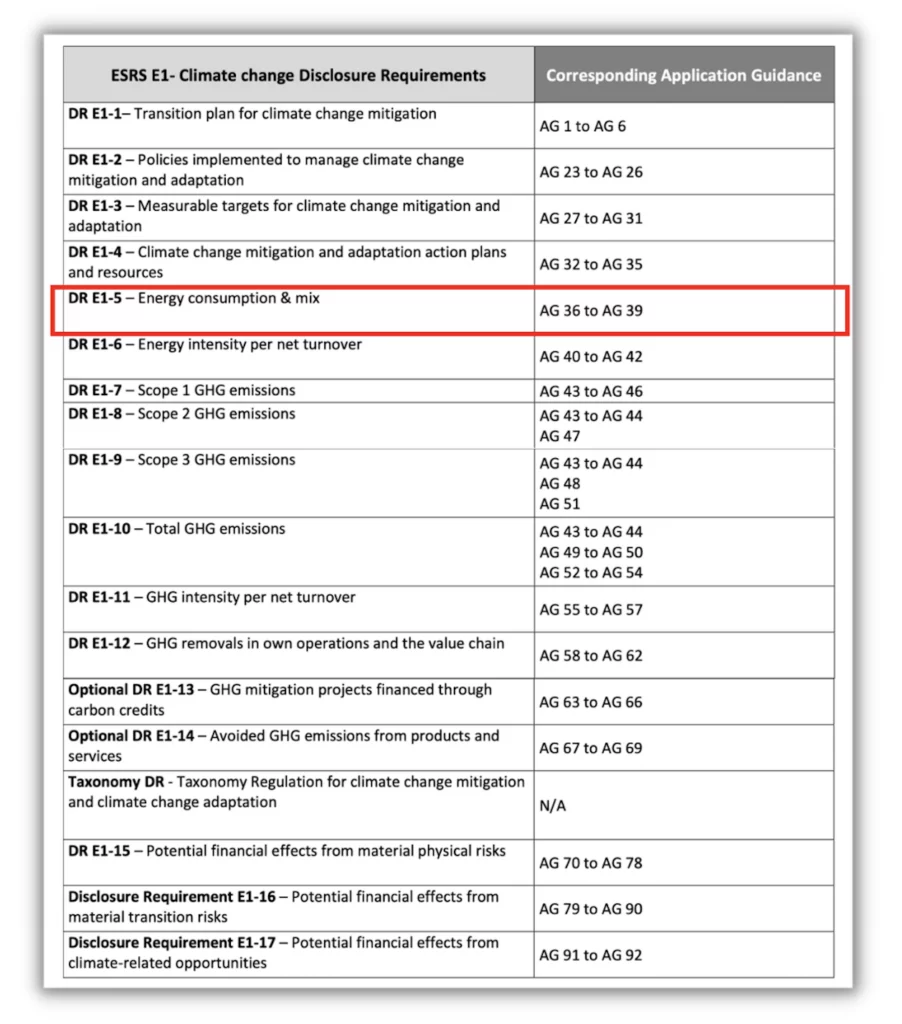

To give the reader some guidance on this complex 'taxonomy', EFRAG has also published the document 'Navigating the ESRS' as Appendix I. Table 3 of this document contains an overview of all Disclosure Principles and Requirements for each ESRS and the corresponding Application Guidance. Based on this overview, we discuss below the example of Disclosure Requirements E1-5, 'Climate change - Energy consumption & mix'.

Example

Disclosure Requirements E1-5 - Energy consumption and mix

To give you a better understanding of exactly what needs to be done, we take the Environment theme - consisting of five ESRS (ESRS E1 to E5) - as an example. This is divided into the following sub-themes:

ESRS E1 - Climate change

ESRS E2 - Pollution

ESRS E3 - Water and marine resources

ESRS E4 - Biodiversity and ecosystems

ESRS E5 - Resource use and circular economy

Based on the overview included below, it becomes clear that the first sub-theme Climate change is again 'cut up' into 17 Disclosure Requirements (DR E1-1 to E1-17). Of these, two are optional. This means you must report on at least 15 different climate-related topics. As an example, we highlight DR E1-5 Energy consumption & mix for you.

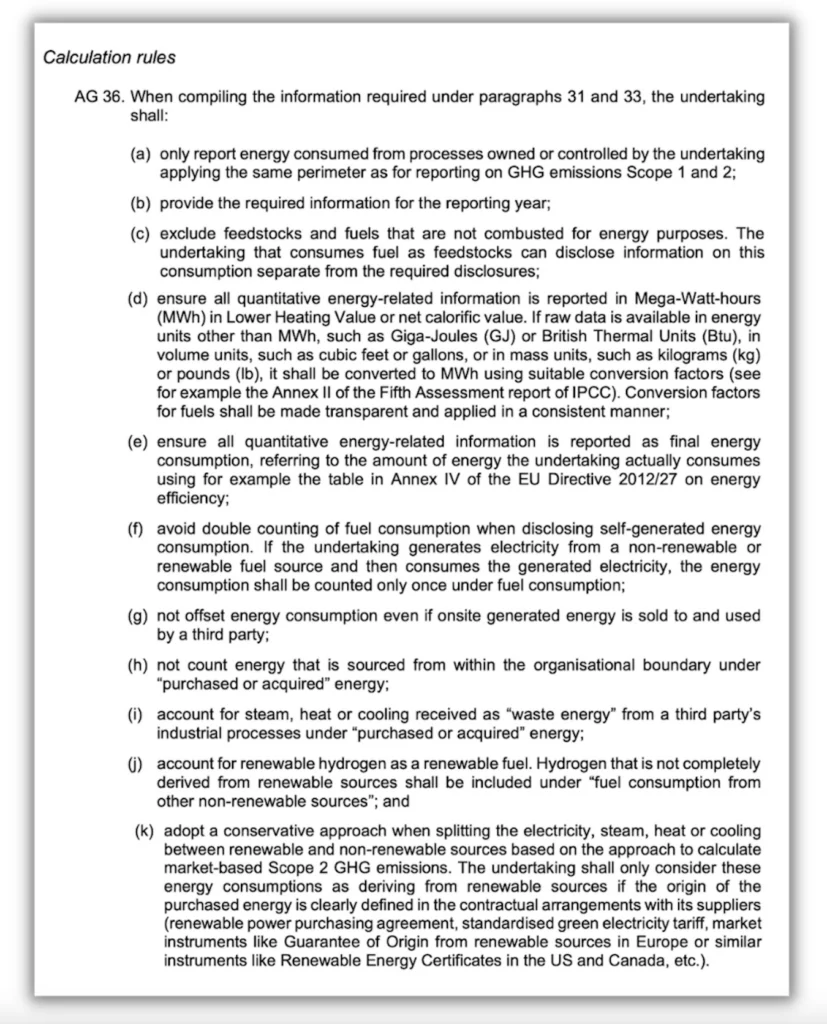

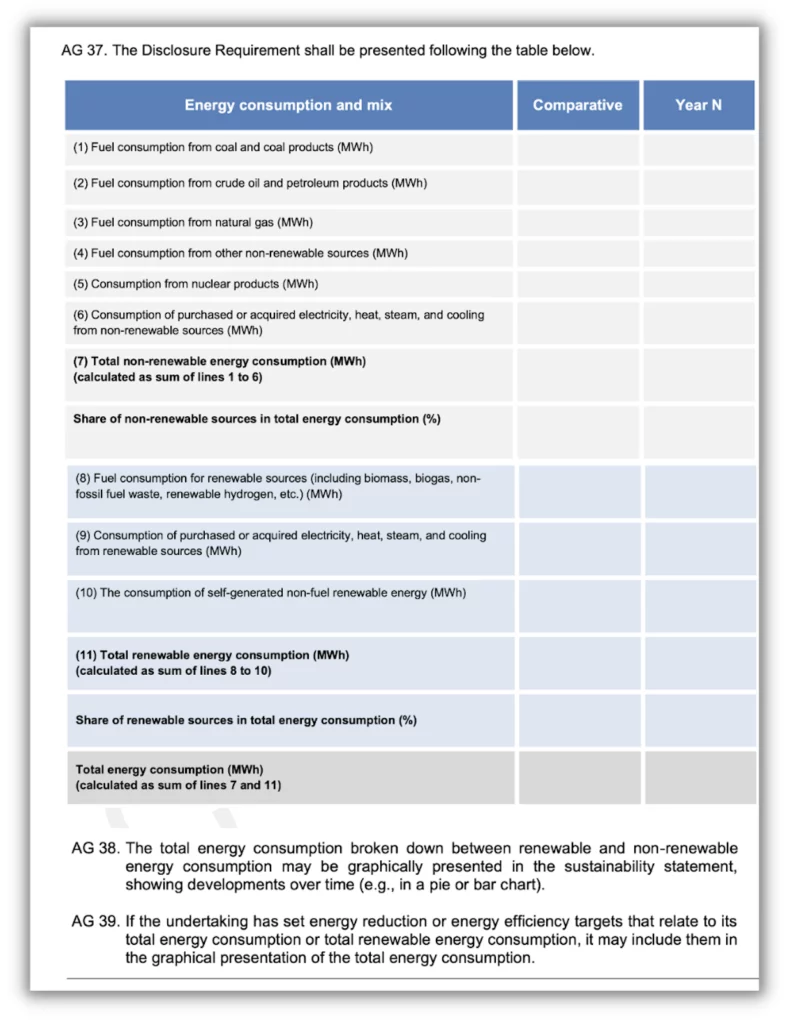

What does this reporting entail? We show that below using the elaborated Disclosure Requirement and corresponding Application Guidance. In brief, it shows that the company must provide information on its total energy consumption, both from non-renewable sources (energy from fossil fuels such as natural gas, oil and coal and nuclear energy) and renewable sources (energy from wind, hydropower, solar, soil, outdoor heat and biomass). The Disclosure Requirement specifies how this energy consumption is to be calculated (calculation rules) and presented.

Using this example, it becomes clear that EFRAG has set the bar high when it comes to providing information on total energy consumption & mix by companies. The same high level of ambition is also visible in the other 136 Disclosure Requirements.

We see two major challenges here:

the availability and quality of data required for sustainability reporting; and

the organisation required to ensure that the company demonstrably meets all sustainability reporting requirements.

Conclusion

EFRAG submitted an ambitious consultation package to the market in April this year. As we noted in a previous article, the draft ESRS evoked some resistance. For instance, regulator AFM indicated that:

the size and complexity of current concepts "hinder feasibility";

users of sustainability information can "lose sight of the forest for the trees" due to too detailed information; and

the rules are thus less verifiable for auditors and regulators, "which increases the risk of greenwashing."

The big question now is what EFRAG will do with the results of its consultation. Assuming that it will want to maintain the 'taxonomy' used for the draft ESRS as much as possible, it faces major challenges. The example mentioned above shows that the availability and quality of sustainability data is one of these challenges.

What can we do for you?

The CSRD and underlying ESRS are 'only' proposals at present. Of course, this does not mean that you should not prepare for their entry into force.

Want to know more about the CSRD? In our CSRD Awareness e-learning, we elaborate in outline how the CSRD works. Upon completion, you will know what requirements your company must meet and when.

Our consultants will be happy to help you on your way to a sustainability report that meets all the requirements of the CSRD and ESRS. Read more about our services or contact us to discuss your specific consulting needs.